“Bible-Based Responses

To

Your Financial Questions”

Here is a bit about what you can expect from this blog. Money is perhaps the least understood yet most discussed topic in our society today. Thousands of families daily make financial decisions based on bad advice.

In reality, the only totally reliable spiritual and financial advice comes from God’s Word–the Bible. I have found that the Bible addresses virtually every financial decision you or I will ever have to make. This Blog is dedicated to help you make those financial decisions–whether great or small. Here you will find many of the financial questions folks ask every day, along with Bible-based responses. These questions and responses are based on materials, publications, and my personal experiences gleaned from 33 years of prayerful service as a certified teacher, trainer, counselor, and/or coach representing the Dave Ramsey organization, the John Maxwell Team, Crown Ministries, and Christian Financial Concepts (Mr. Larry Burkett).

Our 501-c-3 non-profit ministry is Christian Financial Ministries(www.christianfinancialministries.org). We offer you the Holy Spirit inspired and led, Bible-based, Financial Freedom God’s Way Online Academy. Our motto is “Financial Freedom God’s Way: learn it, live it, and lead others to it.”

So, please scroll down, read, share with others, and be blessed in the Lord!

Question: Ever since my divorce, my children and I have really been struggling to make ends meet. Their father supports the children, but only modestly. He sometimes works, but most of the time does not. I find that I just don’t earn enough to make it on a month-to-month basis. Do you have any advice? Response: First, you need to get some financial coaching to be sure you are doing the most with what you have. I suggest www.crown.org, www.daveramsey.com, or www.christianfinancialministries.org. You can also share your needs with your church. Most people in need would find this hard to do and even a bit embarrassing–most would rather not ask for help. That is unfortunate. It is amazing that so many Christians feel the liberty to stand up in church and ask others to pray about an illness, but do not feel they have the right to stand up and ask for financial help. Why? One reason is that Satan has duped us into believing that money is his domain. However, part of God’s financial plan ( 2 Corinthians 8:14 and many others) is for His people to help meet the needs of others. There is help to be had. A good Christian financial coach and your church can help point you to the help you need—if you ask.

Question: Bob, if God does not want Christians to go into debt, does that make a home mortgage wrong? Response: Great question Peggy. Recall from several of our times together here and on the radio, you discovered that God’s Word does not prohibit borrowing. Yet, most young couples need to borrow to buy a house—they need a mortgage. The problem is that a home loan often results in what the Bible calls surety, which is taking on debt without a sure way to repay. Avoiding surety is a biblical principle; it is not biblical law. It is a biblical principle that if ignored may result in some significant negative consequences. For example, if you borrow to buy a home, then if for whatever reason, you cannot afford the mortgage payments, the bank will repossess and sell your home. If the sale price is less than you owe, you will not only lose your home, you will also need to sacrifice other assets to pay the difference between the sale price and the amount remaining on your mortgage. Ouch! So, what can you do? You can prayerfully work to avoid the consequences of surety by making certain that your home is worth more than what you owe. How? First, only borrow to buy a home based on what your cash flow will support–this means you must be living on a budget. Second, make a commitment to quickly reduce your mortgage to the point the house is worth more than you owe. Finally, get some help–do some homework to figure out how to pay off your mortgage as early as possible.

Question: I’m from a school of thought that says use other people’s money (OPM); in other words, borrow to do whatever you want. it’s a hard mentality to shake, even though I now understand it’s contrary to God’s Word. I was recently at a meeting in which fundraisers recommended that people in a congregation borrow to give to the church building program. That sounds more reasonable to me than the church itself borrowing. What do you think? Response: Larry Burkett once wrote, “If you knowingly violate biblical principles, it’s wrong, no matter how noble the purpose. I don’t believe God would direct anyone to violate His Word to accomplish His work. The principle of surety says that we’re not to borrow against an unknown contingency. The idea of using other people’s money has been greatly overplayed in our society, especially within the church. I believe that God has provided us Christians all the money necessary to do anything we want if we are committed to it. Borrowing should never play a part in giving. We should always give what belongs to us, not what belongs to somebody else.” Thank you yet again Larry! I agree–do not borrow to give to your church.

Question:As my teenagers grow toward independence, they will be deluged with credit card offers. I’m concerned that they will get trapped by easy credit. What can I do now to help prevent problems in the future? Response:You can prayerfully begin to teach your older children how to handle credit and credit cards by letting them each have and use their own credit card while still home. “Ouch! Now wait a minute Bob, I know Dave Ramsey would never agree with you on that—no way.” You’re right, Dave wouldn’t. But hear me out. I don’t think there’s anything inherently wrong with credit cards. It’s how they’re used or misused that creates the problems. You can allow your children, sixteen or older, to each have a single credit card if you set and enforce some simple rules. What rules? Let me suggest five. First, they need an income from either a job or an allowance (that’s a topic for another time). Second, set maximum credit card limits as you, your spouse, and your children agree. Three, don’t let them use their cards for anything that is not in their budget—their written budget. This means they must have and be living on a written budget before they get the credit card. Four, they must pay off the entire balance each month. Fifth and finally, the first time they can’t pay the complete balance when the bill comes due, you destroy the card, and not allow them to have a new card for one year. If you prayerfully work with your children to set and faithfully enforce these five simple credit card rules now, your children are unlikely to have credit card problems as adults. How so? Proverbs 22:6 says, “Train up a child in the way he should go, even when he is old he will not depart from it.” Prayerfully set fair rules and enforce them consistently.

Question: Should I claim what I give to God as a deduction on my income tax since God said that I’m to give in secret? Response: It’s highly doubtful that anyone claims a tax deduction because he wants the government to “see” how righteous and generous he is. Besides, the tax return is a private document, and most churches and charitable organizations take great care in keeping donations confidential. The tax deduction is a legitimate benefit that the government has made available to all Americans, and there’s a sense in which it would be poor stewardship not to take advantage of it. The point here is not “secret giving” but rather the wisest possible use of the resources God has entrusted to our care. We are to avoid paying taxes whenever legally possible. We are never to evade paying taxes that are legally required. Claiming your tithe in order to reduce your taxes is good stewardship.

Question:My husband and I have about $14,000 in undergraduate school loans still unpaid. We will accumulate about another $60,000 of debt if we go to graduate school. Do you think it would be better for us to pay off our undergraduate school loans before going to graduate school? Response: With the exception of a few chosen careers, it will be very hard, even with both of you working, to repay $75,000 in school loans. What happens if you have children and want to stay home with them? Then you would lose your income and make it even harder to pay on those loans. My personal thought is not to accumulate that much debt. One of you, preferably your husband, should go back to school part-time. Stretch out the education over a longer period of that so that, rather than accumulating so much debt, you accumulate only a minimum amount. Some graduate schools make provisions for working adults to go part-time, until they have accumulated all but one year of credit hours—then go to school full-time for one year. As a result, that total indebtedness will probably be closer to $10,000 than to $60,000 and will make it much easier to pay back those loans. Just be very careful about accumulating so much debt. It’s very hard to pay it off. In your case, it would be the equivalent of buying a small home and never being able to live in it—a very tough thing to do.

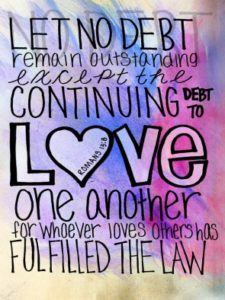

Question: In reading through the Bible, I found Romans 13:8 which says, “Owe nothing to anyone except to love one another; for he who loves his neighbor has fulfilled the law.” Does this mean that God never wants a Christian to borrow money? Response: My interpretation of Romans 13:8 is that the Apostle Paul was not referring directly to money. He was saying, don’t let people do something for you unless you’re willing to do even more for them. If Paul had been specifically telling Christians to never borrow money, I believe He would have made it absolutely clear, because then he would have been countermanding many other Scriptures that deal with borrowing money. In all of the 3,000 or so Bible verses that deal with money, borrowing or lending are not scripturally prohibited. We need to be careful not to build a doctrine out of a single verse but to take Scripture as a whole.

Question: We’ve been on a budget for several months now, but invariably we have a problem when an unexpected expense takes away money that we allocated elsewhere. How do we handle these unexpected expenses? Response: I’ve found that in reality, there are very few unexpected expenses but rather expenses that have not been properly planned for. If you look at your budget on an annual basis, you will find the same “unexpected” expenses reoccur: cars break down, clothing wears out, teeth have holes in them, children get hurt and need medical care, etc. A workable budget must plan for these variables. For example, if you spend $1200 a year on clothing for your family, then $100 a month must be set aside for clothes. In the months you don’t spend that money, it’s not a windfall! It’s an expense that didn’t come due that month; the surplus must be saved for future use. At the end of the month, transfer budgeted but unspent money into a savings account. In any given month there may be unused money in a budget category. If you spend it on other things, your budget will never work. Budgeting is a process of sacrificing short-term spending to accomplish long-term goals. (www.christianfinancialministries.org)

Question: We are parents of a daughter who is engaged. We want her and her husband to enter marriage knowing how to handle money. How do we teach them God’s principles? Response: I suggest they see a trained financial counselor if at all possible (www.daveramsey.com or www.crown.org). If none is available, then help them work through “The total Money Makeover WORKBOOK” (Dave Ramsey) to develop a budget for their first year together. Next, have them demonstrate they both know how to balance a checkbook. Third, discuss the uses of credit and have them promise in writing not to use credit except for budgeted expenses that can be paid off every month—strongly suggest they do not go into debt to pay for their marriage ceremony. Last, have them agree to meet with you at least once a month for the first year to review their budget. By doing these things, you will provide them with good financial counsel. As Proverbs 19:20 says, “Listen to counsel and accept discipline, that you may be wise the rest of your days.” (Note: You can also suggest your daughter and soon-to-be husband become part of our “Financial Freedom God’s Way On-Line Academy” by checking out our website at www.christianfinancialministries.org. )

Question: I keep the home financial records because I have more time than my husband. But I recently heard a Christian financial teacher say that the financial records are the husband’s responsibility. What do you think? Response: It’s been rightfully said that God usually puts opposites together. If a wife has the ability to manage home finances, there is nothing unscriptural about her doing just that. Both husband and wife should develop their financial plans together, however, so that she is not required to make all the decisions. If there are financial problems, especially delinquent bills, the husband should take charge and work out arrangements with creditors. As the authority in the home, he should bear the emotional pressures of creditor harassment. “Husbands, love your wives, just as Christ also loved the church and gave Himself up for her” (Eph. 5:25). In the final analysis, if you’re the better bookkeeper, keep the books.

, the only totally reliable spiritual and financial advice comes from God’s Word–the Bible. I have found that the Bible addresses virtually every financial decision you or I will ever have to make. This Blog is dedicated to help you make those financial decisions–whether great or small. Here you will find many of the financial questions folks ask every day, along with Bible-based responses. These questions and responses are based on materials, publications, and my personal experiences gleaned from 33 years of prayerful service as a certified teacher, trainer, counselor, and/or coach representing the Dave Ramsey organization, the John Maxwell Team, Crown Ministries, and Christian Financial Concepts (Mr. Larry Burkett).

, the only totally reliable spiritual and financial advice comes from God’s Word–the Bible. I have found that the Bible addresses virtually every financial decision you or I will ever have to make. This Blog is dedicated to help you make those financial decisions–whether great or small. Here you will find many of the financial questions folks ask every day, along with Bible-based responses. These questions and responses are based on materials, publications, and my personal experiences gleaned from 33 years of prayerful service as a certified teacher, trainer, counselor, and/or coach representing the Dave Ramsey organization, the John Maxwell Team, Crown Ministries, and Christian Financial Concepts (Mr. Larry Burkett).

es not want Christians to go into debt, does that make a home mortgage wrong? Response: Great question Peggy. Recall from several of our times together here and on the radio, you discovered that God’s Word does not prohibit borrowing. Yet, most young couples need to borrow to buy a house—they need a mortgage. The problem is that a home loan often results in what the Bible calls surety, which is taking on debt without a sure way to repay. Avoiding surety is a biblical principle; it is not biblical law. It is a biblical principle that if ignored may result in some significant negative consequences. For example, if you borrow to buy a home, then if for whatever reason, you cannot afford the mortgage payments, the bank will repossess and sell your home. If the sale price is less than you owe, you will not only lose your home, you will also need to sacrifice other assets to pay the difference between the sale price and the amount remaining on your mortgage. Ouch! So, what can you do? You can prayerfully work to avoid the consequences of surety by making certain that your home is worth more than what you owe. How? First, only borrow to buy a home based on what your cash flow will support–this means you must be living on a budget. Second, make a commitment to quickly reduce your mortgage to the point the house is worth more than you owe. Finally, get some help–do some homework to figure out how to pay off your mortgage as early as possible.

es not want Christians to go into debt, does that make a home mortgage wrong? Response: Great question Peggy. Recall from several of our times together here and on the radio, you discovered that God’s Word does not prohibit borrowing. Yet, most young couples need to borrow to buy a house—they need a mortgage. The problem is that a home loan often results in what the Bible calls surety, which is taking on debt without a sure way to repay. Avoiding surety is a biblical principle; it is not biblical law. It is a biblical principle that if ignored may result in some significant negative consequences. For example, if you borrow to buy a home, then if for whatever reason, you cannot afford the mortgage payments, the bank will repossess and sell your home. If the sale price is less than you owe, you will not only lose your home, you will also need to sacrifice other assets to pay the difference between the sale price and the amount remaining on your mortgage. Ouch! So, what can you do? You can prayerfully work to avoid the consequences of surety by making certain that your home is worth more than what you owe. How? First, only borrow to buy a home based on what your cash flow will support–this means you must be living on a budget. Second, make a commitment to quickly reduce your mortgage to the point the house is worth more than you owe. Finally, get some help–do some homework to figure out how to pay off your mortgage as early as possible. Response: Larry Burkett once wrote, “If you knowingly violate biblical principles, it’s wrong, no matter how noble the purpose. I don’t believe God would direct anyone to violate His Word to accomplish His work. The principle of surety says that we’re not to borrow against an unknown contingency. The idea of using other people’s money has been greatly overplayed in our society, especially within the church. I believe that God has provided us Christians all the money necessary to do anything we want if we are committed to it. Borrowing should never play a part in giving. We should always give what belongs to us, not what belongs to somebody else.” Thank you yet again Larry! I agree–do not borrow to give to your church.

Response: Larry Burkett once wrote, “If you knowingly violate biblical principles, it’s wrong, no matter how noble the purpose. I don’t believe God would direct anyone to violate His Word to accomplish His work. The principle of surety says that we’re not to borrow against an unknown contingency. The idea of using other people’s money has been greatly overplayed in our society, especially within the church. I believe that God has provided us Christians all the money necessary to do anything we want if we are committed to it. Borrowing should never play a part in giving. We should always give what belongs to us, not what belongs to somebody else.” Thank you yet again Larry! I agree–do not borrow to give to your church. working, to repay $75,000 in school loans. What happens if you have children and want to stay home with them? Then you would lose your income and make it even harder to pay on those loans. My personal thought is not to accumulate that much debt. One of you, preferably your husband, should go back to school part-time. Stretch out the education over a longer period of that so that, rather than accumulating so much debt, you accumulate only a minimum amount. Some graduate schools make provisions for working adults to go part-time, until they have accumulated all but one year of credit hours—then go to school full-time for one year. As a result, that total indebtedness will probably be closer to $10,000 than to $60,000 and will make it much easier to pay back those loans. Just be very careful about accumulating so much debt. It’s very hard to pay it off. In your case, it would be the equivalent of buying a small home and never being able to live in it—a very tough thing to do.

working, to repay $75,000 in school loans. What happens if you have children and want to stay home with them? Then you would lose your income and make it even harder to pay on those loans. My personal thought is not to accumulate that much debt. One of you, preferably your husband, should go back to school part-time. Stretch out the education over a longer period of that so that, rather than accumulating so much debt, you accumulate only a minimum amount. Some graduate schools make provisions for working adults to go part-time, until they have accumulated all but one year of credit hours—then go to school full-time for one year. As a result, that total indebtedness will probably be closer to $10,000 than to $60,000 and will make it much easier to pay back those loans. Just be very careful about accumulating so much debt. It’s very hard to pay it off. In your case, it would be the equivalent of buying a small home and never being able to live in it—a very tough thing to do. mean that God never wants a Christian to borrow money? Response: My interpretation of Romans 13:8 is that the Apostle Paul was not referring directly to money. He was saying, don’t let people do something for you unless you’re willing to do even more for them. If Paul had been specifically telling Christians to never borrow money, I believe He would have made it absolutely clear, because then he would have been countermanding many other Scriptures that deal with borrowing money. In all of the 3,000 or so Bible verses that deal with money, borrowing or lending are not scripturally prohibited. We need to be careful not to build a doctrine out of a single verse but to take Scripture as a whole.

mean that God never wants a Christian to borrow money? Response: My interpretation of Romans 13:8 is that the Apostle Paul was not referring directly to money. He was saying, don’t let people do something for you unless you’re willing to do even more for them. If Paul had been specifically telling Christians to never borrow money, I believe He would have made it absolutely clear, because then he would have been countermanding many other Scriptures that deal with borrowing money. In all of the 3,000 or so Bible verses that deal with money, borrowing or lending are not scripturally prohibited. We need to be careful not to build a doctrine out of a single verse but to take Scripture as a whole. n: We’ve been on a budget for several months now, but invariably we have a problem when an unexpected expense takes away money that we allocated elsewhere. How do we handle these unexpected expenses? Response: I’ve found that in reality, there are very few unexpected expenses but rather expenses that have not been properly planned for. If you look at your budget on an annual basis, you will find the same “unexpected” expenses reoccur: cars break down, clothing wears out, teeth have holes in them, children get hurt and need medical care, etc. A workable budget must plan for these variables. For example, if you spend $1200 a year on clothing for your family, then $100 a month must be set aside for clothes. In the months you don’t spend that money, it’s not a windfall! It’s an expense that didn’t come due that month; the surplus must be saved for future use. At the end of the month, transfer budgeted but unspent money into a savings account. In any given month there may be unused money in a budget category. If you spend it on other things, your budget will never work. Budgeting is a process of sacrificing short-term spending to accomplish long-term goals. (www.christianfinancialministries.org)

n: We’ve been on a budget for several months now, but invariably we have a problem when an unexpected expense takes away money that we allocated elsewhere. How do we handle these unexpected expenses? Response: I’ve found that in reality, there are very few unexpected expenses but rather expenses that have not been properly planned for. If you look at your budget on an annual basis, you will find the same “unexpected” expenses reoccur: cars break down, clothing wears out, teeth have holes in them, children get hurt and need medical care, etc. A workable budget must plan for these variables. For example, if you spend $1200 a year on clothing for your family, then $100 a month must be set aside for clothes. In the months you don’t spend that money, it’s not a windfall! It’s an expense that didn’t come due that month; the surplus must be saved for future use. At the end of the month, transfer budgeted but unspent money into a savings account. In any given month there may be unused money in a budget category. If you spend it on other things, your budget will never work. Budgeting is a process of sacrificing short-term spending to accomplish long-term goals. (www.christianfinancialministries.org) WORKBOOK” (Dave Ramsey) to develop a budget for their first year together. Next, have them demonstrate they both know how to balance a checkbook. Third, discuss the uses of credit and have them promise in writing not to use credit except for budgeted expenses that can be paid off every month—strongly suggest they do not go into debt to pay for their marriage ceremony. Last, have them agree to meet with you at least once a month for the first year to review their budget. By doing these things, you will provide them with good financial counsel. As Proverbs 19:20 says, “Listen to counsel and accept discipline, that you may be wise the rest of your days.” (Note: You can also suggest your daughter and soon-to-be husband become part of our “Financial Freedom God’s Way On-Line Academy” by checking out our website at

WORKBOOK” (Dave Ramsey) to develop a budget for their first year together. Next, have them demonstrate they both know how to balance a checkbook. Third, discuss the uses of credit and have them promise in writing not to use credit except for budgeted expenses that can be paid off every month—strongly suggest they do not go into debt to pay for their marriage ceremony. Last, have them agree to meet with you at least once a month for the first year to review their budget. By doing these things, you will provide them with good financial counsel. As Proverbs 19:20 says, “Listen to counsel and accept discipline, that you may be wise the rest of your days.” (Note: You can also suggest your daughter and soon-to-be husband become part of our “Financial Freedom God’s Way On-Line Academy” by checking out our website at  Question: I keep the home financial records because I have more time than my husband. But I recently heard a Christian financial teacher say that the financial records are the husband’s responsibility. What do you think? Response: It’s been rightfully said that God usually puts opposites together. If a wife has the ability to manage home finances, there is nothing unscriptural about her doing just that. Both husband and wife should develop their financial plans together, however, so that she is not required to make all the decisions. If there are financial problems, especially delinquent bills, the husband should take charge and work out arrangements with creditors. As the authority in the home, he should bear the emotional pressures of creditor harassment. “Husbands, love your wives, just as Christ also loved the church and gave Himself up for her” (Eph. 5:25). In the final analysis, if you’re the better bookkeeper, keep the books.

Question: I keep the home financial records because I have more time than my husband. But I recently heard a Christian financial teacher say that the financial records are the husband’s responsibility. What do you think? Response: It’s been rightfully said that God usually puts opposites together. If a wife has the ability to manage home finances, there is nothing unscriptural about her doing just that. Both husband and wife should develop their financial plans together, however, so that she is not required to make all the decisions. If there are financial problems, especially delinquent bills, the husband should take charge and work out arrangements with creditors. As the authority in the home, he should bear the emotional pressures of creditor harassment. “Husbands, love your wives, just as Christ also loved the church and gave Himself up for her” (Eph. 5:25). In the final analysis, if you’re the better bookkeeper, keep the books.